Retirement Income Review

By Next Wealth | 22 March 2024 | 6 minute read

The Financial Conduct Authority (FCA) has this week written to the Chief Executives of financial advice firms asking them to review their processes when providing retirement income advice following the findings from a thematic review of retirement income advice.

There is a very clear call to action here, and it seems the FCA has gone as far as it can in setting out its expectations.

This is another example of the true effect of Consumer Duty and how the regulator sees the Duty underpinning everything in relation to how financial advice is delivered to UK consumers. Unlike the RDR (retail distribution review), which set a very high level of expectation, the AGBR (advice guidance boundary review) and now RIR (retirement income review) leave nothing to interpretation.

The regulator has been very clear in its messaging that anyone providing and charging for financial advice has to provide demonstrable evidence of not just the recommendation (the suitability letter) but the process of making those recommendations.

In particular and in relation to this RIR, advisers must outline the risks to overcome or point out where there might be any associated harm. Associated harm is an important choice of words because it broadens the boundaries to capture all possibilities. The regulator also uses the term “….and long into the future,” which screams ‘ongoing suitability of advice” and that there is no such thing as “simple” retirement income advice.

The Dear CEO letter sent to advice firms was very clear. Review and act, in other words ‘make it right’. Clearly, when the FCA kicked off the thematic review, it was with this in mind – gather the facts, evidence and point them out, and demand change.

The not-so-good practices (without going into detail on all of them) said to me that there were several processes which need refining. Assessing clients’ attitudes to risk is one of them. ATRQs simply aren’t doing enough to support clients in decumulation. Several times in the review, it stated that, too often, it was hard to distinguish different processes for accumulation/decumulation.

During our research with Just [Guarding Financial Futures] we asked more than 200 advice professionals about their approach to determining and reviewing clients’ risk levels, their use of tools, and mapping of risk profiles to investment solutions. Our findings were – it varies. It often comes down to the adviser and is a personal discussion.

This is exactly a point made by the regulator as an area needing improvement, and if you (the advice firm), after a review of your processes, don’t meet the benchmark, then you’d better change it and make sure those providing the advice know about it and are measured on it.

The regulator wants to see the process; it needs to stack up as a process, and it needs to be monitored. In our Future of Financial Advice research, we spoke to 30 business leaders about their future plans and predictions, and all had regulation at the top of the list. One of our hypotheses at the start of that research was that there would be a nationalisation of networks that drive consistent frameworks, including tech and product-led decision-making. The MD of a financial planni

ng firm told us, “Under Consumer Duty, we possibly need to change the way we’re doing business” – is this the start?

Two things struck me.

- Business models for advice delivery. In our Future of Financial Advice research, we predicted that in the next 5 years we will see different business models emerge with six distinct segments of adviser businesses. Firms are already grappling with where they position themselves, what they charge for (and what they don’t), and the operating modeland structure (re)alignment. This may lead to a further overhaul of the commercials of these businesses.

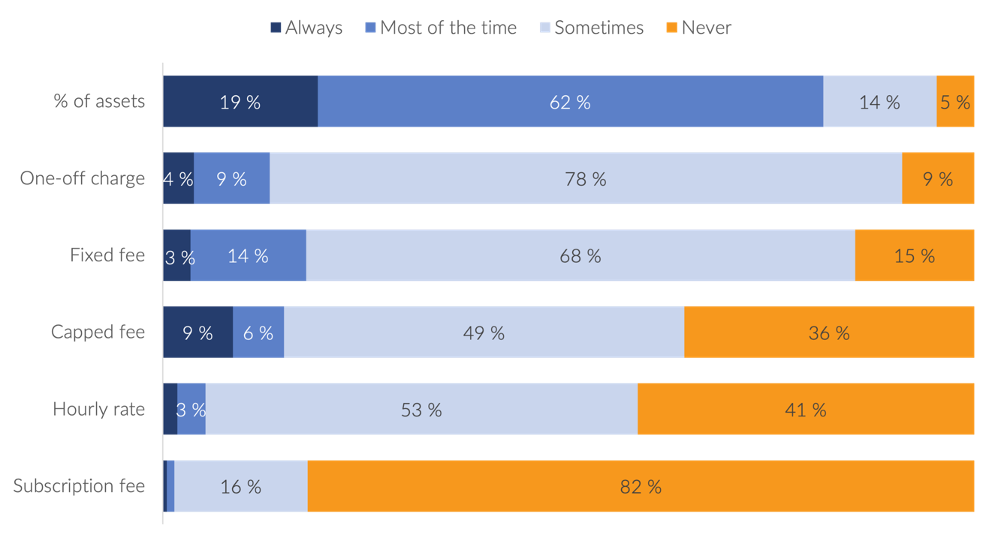

2. Advice charge. We have already seen some progressive movements by advice firms towards fixed fee and subscription-based models.

What does this do to those firms [80%] who are still charging % of assets? Suddenly the cost to deliver retirement advice just got higher. On average from our annual Financial Advice

Business Benchmarks research 75% of advisers charge an initial fee with an average of 0.64% ongoing. This will go up (and up, and up) if we don’t find new ways of working. That would certainly be a serious unintended consequence of strong-arm regulation, which might backfire.

My final point is on cashflow modelling . The regulator wrote an article on this, and it’s quite to the point – you need to stand behind the output, not just accept it. I suspect this isn’t just aimed at cashflow modelling either.

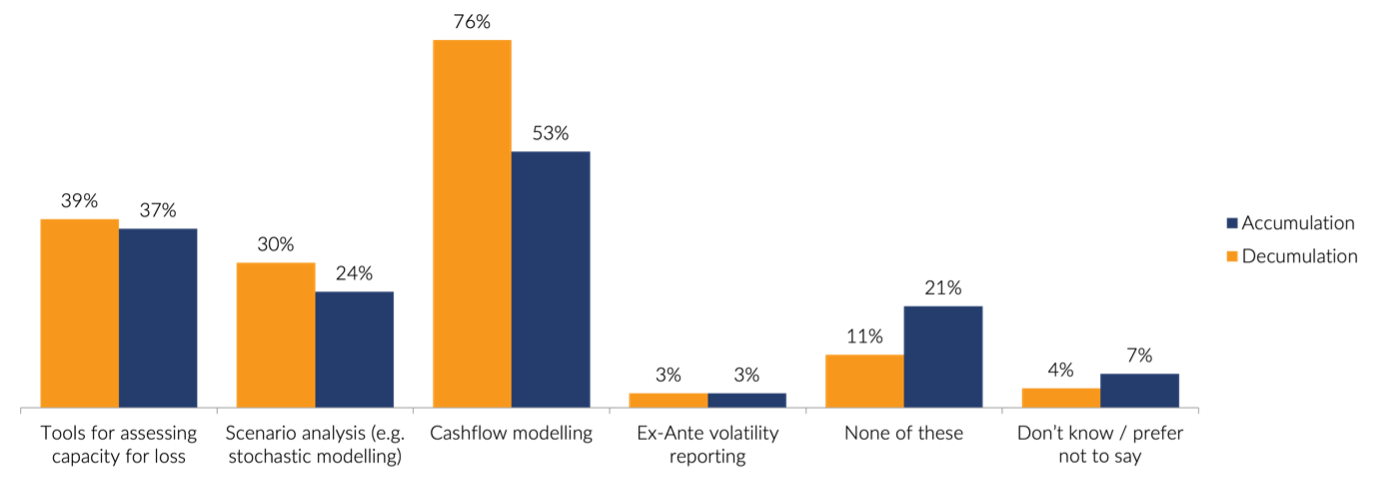

This is rather specific and a huge callout to those who don’t yet use tools for assessing risk. For example in our research 81% of financial advisers use cash flow modelling when giving retirement advice (Source: Managing Lifetime Wealth report sponsored by Aegon). Roughly a one third use tools for capacity for loss and even less than that for scenario analysis when giving retirement income advice (Source Guarding Financial Futures research sponsored by Just).

Which of the following tools do you use for assessing risk?

Source: Guarding Financial Futures NextWealth report sponsored by Just, November 2023

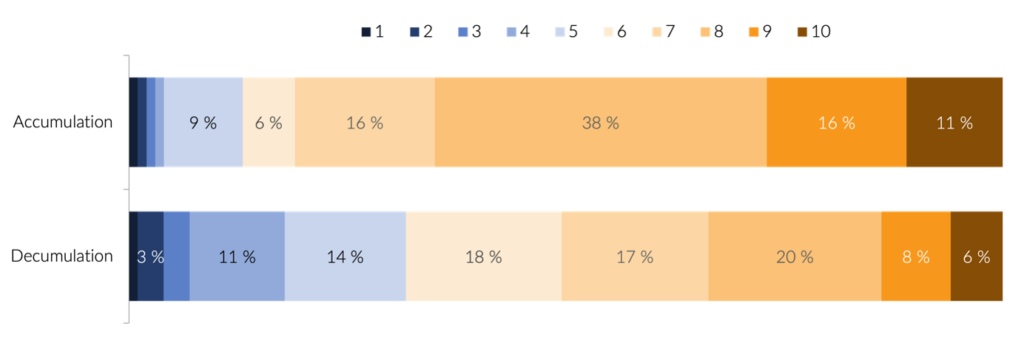

Looking at the ATRQ and its importance or value in the advice process, and in the decumulation of assets phase, advice professionals told us they didn’t value the questionnaire much at all (only a third gave it an 8 out of 10 or better) . Combining ATRQ, CFL (capacity for loss) and CFP (cashflow planning) is going to be extremely difficult when in many cases these systems don’t talk to each other.

On a scale of 1 to 10, how effective is the attitude to risk questionnaire in assessing risk for clients in accumulation and decumulation?

Source: Guarding Financial Futures NextWealth report sponsored by Just, November 2023

Without specifying the specific do’s and don’t’s, the FCA was rather explicit in its expectations.

Do

- Use jusifiable rates of return

- Take account and plan for uncertainty

- Make sure the customer understands and can correctly interpret the output

- Take account of past and future expenditures and desired lifestyle

- Justify any estimated figures

- Use up to date market values

- Determine single or joint life scenarios

- Consideration of tax

Don’t

- Rely on outputs without consideration of the accuracy

- Use unrealistic forecast projections

There is no doubt about it. Our world is changing.

“The future is created in incremental moments small changes, new capabilities and the introduction here and there of different ways of thinking and operating, such that when we look around in 2028 it may feel that nothing has really changed. But when we look back, everything has.” Heather Hopkins, NextWealth

Emma