Financial Advice Market Trends UK

By Next Wealth | 24 July 2020 | 4 minute read

The below figures have been updated in 2022, you can read more here.

The FCA has published a data bulletin with trends and data on the financial adviser market, based on RMAR filings. The following is a summary of some key takeaways.

Headline findings:

- More advisers, fewer firms. The good news is that adviser numbers are creeping upward, slowly. The trend to consolidation is not yet clear in the data.

- SME’s continue to dominate. 89% of firms have five or fewer financial advisers – the same figure as for the past four years.

- The steady decline in the proportion of advisers that are restricted continues.

- Firms with between six and fifty advisers continue to earn more per advisers than either larger or smaller firms. But the rate of growth of revenue per adviser took a turn for the worse this year suggesting their lead on productivity is declining.

- PII Premiums were up 2% as a proportion of revenue in 2019.

- Charges based on a percentage of assets continue to dominate both on-going and initial fees.

More advisers, fewer firms (again)

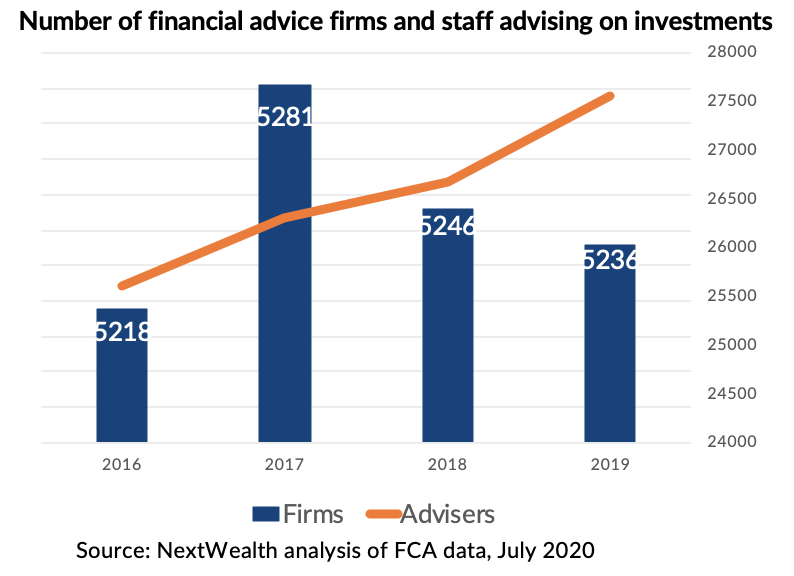

There were 27,557 financial advisers in the UK in 2019, up 3% year on year and up 8% since 2016. The chart below shows the number of financial advisers and number of firms over the past four years.

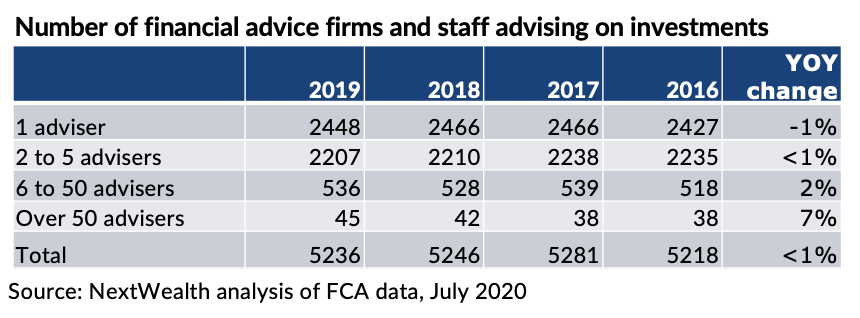

SMEs continue to dominate the financial advice market: 89% of financial advice firms have five or fewer advisers. The share of firms with five or fewer advisers has remained unchanged in the past four years.

While there is a constant drumbeat of speculation about consolidation of the advice market, the numbers tell a different story. The decrease in the number firms, may appear stark on the graph, but represents less than a 1% decrease year on year. We continue to see a slow and steady decrease in the number of small firms and a slow and steady rise in the number of big firms. But the numbers are too small to call it a structural change in the market. Note that the number of large firms is small and so the percentage increase appears much larger. The table below shows the number of firms by number of advisers over time.

There has been a slow and steady increase in the proportion of advisers that are independent and a slow and steady decrease in the proportion that are restricted.

Five to Fifty Sweet Spot

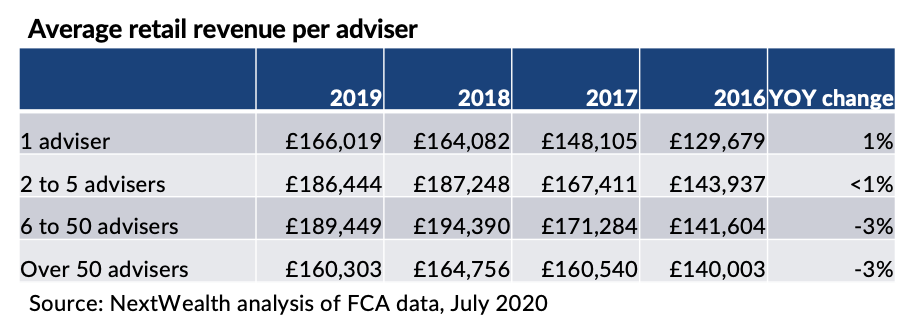

Last year, we said that firms with between five and fifty advisers continue to make more money per adviser than either smaller or larger firms. We noted that revenue growth year on year is also greater – strengthening their lead. Again this year, firms with between six and 50 advisers earned more per adviser than larger or smaller firms. But different from last year, these firms did not enjoy stronger growth in revenue per adviser. Instead this year, revenue per adviser for those mid-size firms decreased year on year (only slightly by 3%). Revenue per adviser also fell for firms with 50 or more advisers. Have adviser firms reached their peak on revenue per adviser? We don’t think so. We still think that mid-sized firms can be more efficient with lower overhead costs than the largest firms. The technology that has been used through the Coronavirus pandemic should help boost productivity for advisers. That said, with revenue largely based on a percentage of assets, market fluctuations will affect revenue per head.

PII Premiums continue to rise as a proportion of revenue

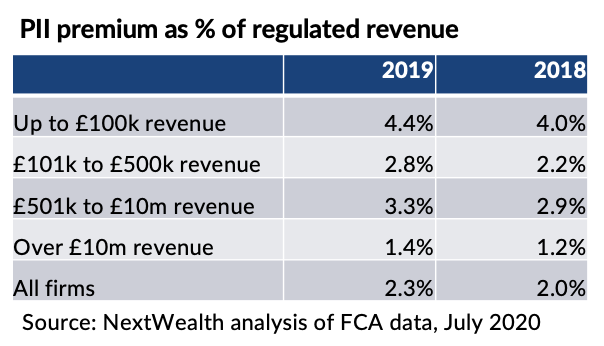

Again this year, PII premiums rose, though the percentage change was only 2%, according to FCA data.

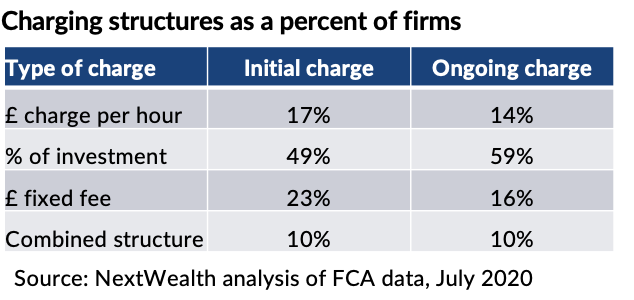

Financial advice charging models

There was virtually no change in the charging models used by financial advisers in 2018 to 2019. The table below shows that charging as a percentage of assets remains the dominant model for both initial and on-going advice. Half of firms charge this way for the initial advice and 59% for on-going advice.

Concluding thoughts

This year’s RMAR data from the FCA show that financial adviser firms continue to be in good financial health with a growing customer base. Financial advice businesses are mostly SMEs and we think many of these firms are struggling to boost productivity and revenue per adviser. With strong processes in place, clear delineation of responsibility and a well integrated tech stack in place, we think firms can adapt and thrive to meet the growing need for quality financial advice and financial planning.

You can read our free Financial Advice Business Benchmarking report for more data and insight on the financial advice market. NextWealth helps advisers to review business processes to boost efficiency and helps fund managers, platforms and technology companies to adapt and change to grow their reach with financial advisers. Get in touch for more information.