Discretionary MPS – VAT charging, market size and pricing pressure

By Next Wealth | 06 January 2021 | 2 minute read

Our latest report shows that assets in discretionary model portfolio services continues to rise but that the growth is uneven. DFMs enjoying above average growth in assets in their models tend to be part of consolidators or are transferring existing assets.

Market size

We estimate that 15% of advised platform assets are in discretionary MPS. This is based on data collected from platforms and through adviser surveys. Adviser managed model portfolios (AMPs) continue to attract far more assets – about half of adviser platform assets are in AMPs. Among the firms profiled, consolidator Fairstone, is fastest growing followed by FE. Morningstar and Quilter Cheviot by contrast, have seen assets decrease year on year. In this report we explore the drivers of this change.

Vertical integration and strategic partnerships

Discretionary MPS is a highly competitive part of the market with intense pricing pressure and a lot of choice. Advisers that use a DFM use an average of between two and three. DFMs part of vertically integrated businesses, consolidators and those with strong strategic partnerships have faired best.

The year’s fastest growing DFMs covered in the research were Fairstone, FE and Wellian. NextWealth research suggests that Fairstone and Wellian’s growth is being fuelled by consolidation and FE’s is a result of moving assets from its template models to the discretionary offering.

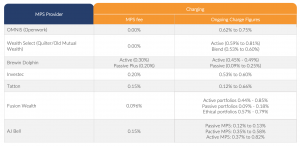

VAT Charging

Cazenove quietly removed VAT from portfolios in January followed more loudly by Tatton in June. There hadlong been a debate as to whether a model portfolio was a product or service and whether VAT should be paid. Cazenove received an exemption early in the year and Tatton received a refund for VAT paid in past years. Other DFMs have been quick to follow suit.

At the end of last year, all DFMs in the NextWealth report charged VAT (though Tatton’s said VAT was included in the DFM fee), this year, 13 DFMs say they don’t charge VAT and a further 6 say it is under review.

Race to Zero

There is an evident race to “zero-cost” MPS in terms of the management of the portfolios. The companies that can, the vertically integrated businesses, are at or near zero; it’s the underlying assets that are providing revenue. The consequences of this are that businesses must differentiate themselves through client experience and investment outcomes, whilst looking to remove cost through efficient technology.

The report is available to purchase. Additional details here.